Your Early Adopters Are Not Your Customers

Not Customers. Launch Partners.

There are platforms I used to recommend without thinking. A few of them aren’t on my list anymore. None of them shipped a worse product. They shipped a different relationship.

Every business book will tell you this is just how it works. The chasm. The math. The price sheet. The textbook says you outgrow your early adopters because you have to.

It doesn’t have to be.

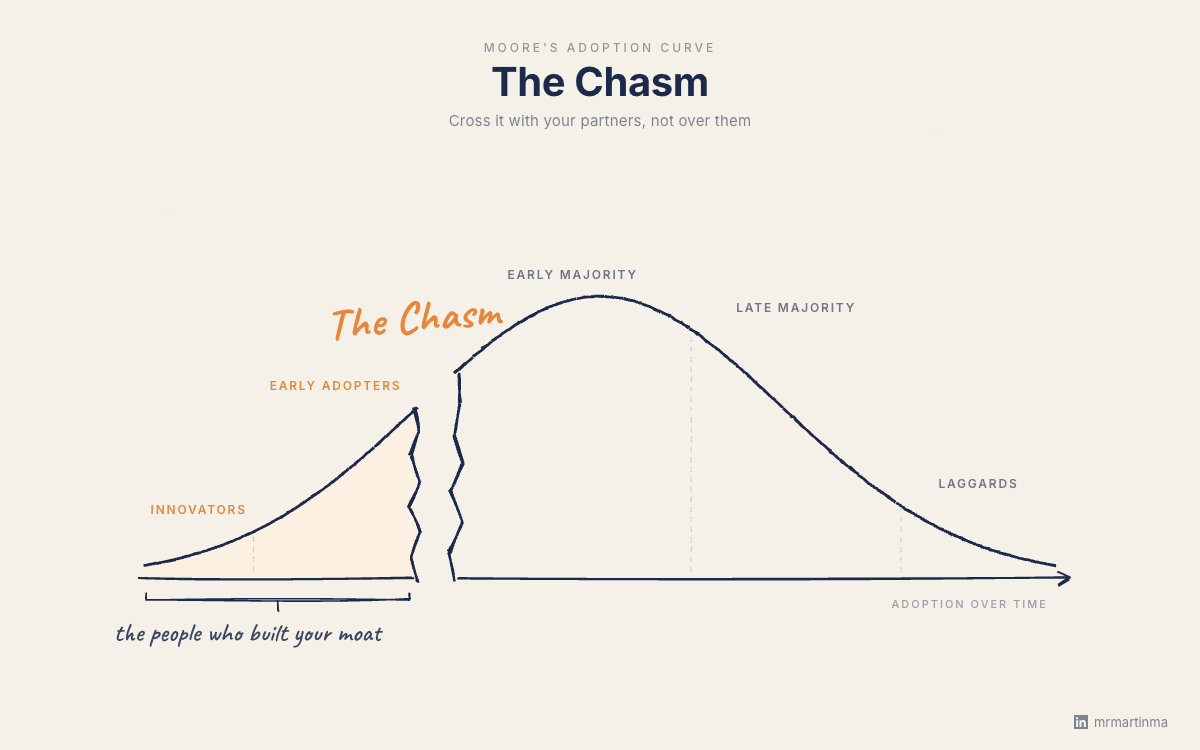

The chasm and the cohort

Geoffrey Moore added the chasm to the adoption curve in 1991. Innovators on the left. Laggards on the right. The chasm in the middle. A generation of platform builders has been crossing it ever since.

Moore taught us how to cross it. The question he left alone was what to do with the people on the near side.

The default move is to leave them. Most platforms do. Shopify, Stripe, Figma, and Supabase didn’t. They crossed anyway, without strip-mining the cohort that built the bridge.

The model that brings early adopters in is almost never the model that pays the bills at scale. So you will evolve. That part isn’t optional. The original promise drew the cohort in because it was generous. That generosity is what eventually has to change.

The real question is what kind of change. You can serve the partners and make money on the same activity. Or you can price them out and make money on what they leave behind. Both are legal. Only one compounds.

Last week I wrote about Costco’s $1.50 hot dog and how value earns the right to enforce a boundary. That post was about how you earn the relationship at the door. This one is about what you owe the people who walked in.

Your early adopters were never your customers. They were the unpaid founding labor that built the moat. The question is whether you’ve architected the business so they’re still standing on it five years from now.

1. Name the people who built your moat. By handle.

The Partner Audit is the diagnostic underneath every monetization decision you’ll make this year.

Before you change a price, change a tier, deprecate an API, stop supporting your open source projects, or rebrand the docs, do you actually know who built the trust the brand is now monetizing? Not the persona deck. The actual list. The Discord regulars, the integration authors, the YC batches who picked you, the volunteer mods, the engineers who push your name in their company’s vendor selection thread.

If the list doesn’t exist, you don’t understand your own moat. You just happen to be on top of it right now.

Tobi Lütke didn’t discover his merchants and agencies were the moat after the fact. He built Shopify around the premise. Amazon competes with sellers; Shopify makes money only when merchants make money. Tens of thousands of apps and thousands of agency partners, two decades in, every pricing decision still gets read against the merchants first.

Name fifty. If the rest of the market wouldn’t feel their absence, the list is wrong, and you’re still working from a persona deck.

2. Every move on the price sheet does one of two things.

Extraction or replenishment. There’s no neutral monetization move.

Take a price increase. If it funds better docs and faster support, the contributors help you launch it. If it funds executive bonuses while their support tickets get slower, they organize a Discord channel called #migration-guide. Or take a paid tier. The volunteer power users will happily buy one they could have built themselves. They will revolt against one retroactively added to what was promised free.

You have to monetize. The real question is whether your top contributors would help you ship the change, or organize against it.

Figma did this in public. Open APIs from day one. Plugin marketplace that doesn’t tax plugin revenue. “Your data is yours” on the company blog. When Adobe tried to buy them for $20B in 2022, the community reaction (plus regulators) killed the deal. Figma kept compounding under the same founder, same promise, same persona. The platform widened the partnership instead of narrowing it.

Reddit went the other way. Calling it greed misses the actual mechanics.

Reddit’s original model genuinely couldn’t pay the late-stage bills. Volunteer mods, third-party developers, an ad-light experience. None of it was producing the margin a public-market exit needed. They had to evolve. They picked the path that priced out the third-party ecosystem and monetized the volunteer mod labor that had built the platform. Eight thousand subreddits went dark in June 2023. The IPO happened anyway. The moat hollowed out and the people who built it left.

I have watched this conversation play out in vendor meetings this quarter. Other paths existed for Reddit. Slower ones, harder ones, ones that didn’t fit the timeline the cap table needed. The point isn’t that Reddit is evil. The point is the path got chosen, and the path made the contributors the asset being sold rather than the asset being served.

3. The platform no one wants to leave is the one they can.

Lock-in built on respect compounds. The kind built on “they have nowhere else to go” defects the moment someone opens a door.

Tailscale published “backward compatible, forever” as a contract on the company blog. Supabase is open source on Postgres; if they ever drifted, the community could host itself elsewhere within a week, and Supabase knows it.

Both are growing faster than their extractive peers. The structural guarantee that exit is available is the thing that makes partners invest in the first place. Design-for-exit isn’t a concession. It’s the feature.

Twitter killed the third-party API in January 2023. The same apps that invented pull-to-refresh. Ad revenue collapsed from $4.1B to $2B in a year. Digg lost 99.75% of its value to Reddit in twenty-three months and the users organized the exodus on the competitor’s site.

Tailscale and Supabase. Crossing the chasm with their partners, not over them. Allbirds didn’t have that option.

The shoe company that became an AI company

Eight days ago, in a category with nothing to do with platforms, the same arc finished playing.

Allbirds, the merino wool sneaker, one of my favorite, that became Silicon Valley’s tech uniform, sold its shoe business for $39M in March. Two weeks later, on April 15, the publicly-traded shell rebranded as “NewBird AI” with $50M to buy GPUs. From a $4B valuation in late 2021. The shoe, the thing the original cohort bought into, has no corporate home anymore. The shell pivoted to whatever the next capital cycle was paying for, which this April happens to be AI compute.

Private equity has industrialized a model where you buy a company, load it with debt, pay yourself back with dividends recapped from its own cash flow, and sell the husk to the next buyer. PE-backed companies go bankrupt at roughly ten times the rate of non-PE-backed peers. You don’t have to look hard to see this in your own industry.

Allbirds didn’t need a PE owner to become NewBird AI. It just needed a public market hungry for GPU exposure and a wool-shoe story that couldn’t deliver the margin. The mechanism is the same regardless of who’s holding the paper. Which is why the architecture decisions in front of you this quarter outlast the cap table pressuring them.

For the consumer-hardware version of this same arc, watch MKBHD on OnePlus. January 2026. Same enthusiast cohort, same pivot away from them, different industry. The mechanism doesn’t care what you sell.

The platform I’m writing on

I run platform teams for a living. I write about platforms on a platform. Both jobs have the same problem in front of them, and the second one made me see the first one more clearly.

The people who’ve been here since Post 001 are not “audience growth.” They’re the cohort that decided this writing was worth coming back to before the metrics did. If I evolve this in a way that prices them out (different audience, different register, different argument), the cap table doesn’t get me. The brand erodes anyway, just one tier earlier.

Same architecture conversation, smaller scale.

You’re reading this because you decided this writing was worth coming back to before the metrics did. That makes you a launch partner. Don’t let me forget it.

Cross the chasm with the people who showed up. Not over them. The platforms that compound figured out a model where the original identity is the profit engine. Shopify makes money when merchants do. Stripe charges per transaction the developer ships. Supabase monetizes hosting on top of free open source. Figma monetizes seats on a tool the community built around. Same identity, scaled. The platforms that didn’t eventually become NewBird AI. A corporate shell on the other side of the chasm, with no one from the original side standing on it.

So here is my question to you: look at the top fifty people who built your moat. If your next big change went out tomorrow, would they help you ship it, or write the migration guide to the alternative?

#Leadership #PlatformEngineering #Strategy #ProductManagement #FutureOfWork